大家好,我是带我去滑雪!

本期利用Google股价数据集,该数据集中GOOG_Stock_Price_Train.csv为训练集,GOOG_Stock_Price_Test.csv为测试集,里面有开盘价、最高股价、最低股价、收盘价、调整后的收盘价、成交量,2021年11月以前,可以在美国Yahoo网站下载股价历史数据,但现在对中国已经禁用了,可以去其他地方进行下载。本次使用调整后的收盘价进行预测。

目录

1、导入相关模块和数据集

2、产生训练所需的特征和标签数据

3、转换数据为(样本数,时步、特征)的张量

4、定义LSTM模型

5、使用已经训练好的LSTM模型预测股价

6、绘制真实股价与预测股价的对比图

1、导入相关模块和数据集

import numpy as np

import pandas as pd

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

from keras.layers import Dense, Dropout,LSTM,SimpleRNN,GRU# 载入Google股价数据集

df_train = pd.read_csv(r'E:\工作\硕士\博客\博客37-\GOOG_Stock_Price_Train.csv',index_col="Date",parse_dates=True)

print(df_train)

df_test = pd.read_csv(r'E:\工作\硕士\博客\博客37-\GOOG_Stock_Price_Test.csv',index_col="Date",parse_dates=True)

print(df_test )输出结果:

Open High Low Close Adj Close \ Date 2012-01-03 324.360352 331.916199 324.077179 330.555054 330.555054 2012-01-04 330.366272 332.959412 328.175537 331.980774 331.980774 2012-01-05 328.925659 329.839722 325.994720 327.375732 327.375732 2012-01-06 327.445282 327.867523 322.795532 322.909790 322.909790 2012-01-09 321.161163 321.409546 308.607819 309.218842 309.218842 ... ... ... ... ... ... 2016-12-23 790.900024 792.739990 787.280029 789.909973 789.909973 2016-12-27 790.679993 797.859985 787.656982 791.549988 791.549988 2016-12-28 793.700012 794.229980 783.200012 785.049988 785.049988 2016-12-29 783.330017 785.929993 778.919983 782.789978 782.789978 2016-12-30 782.750000 782.780029 770.409973 771.820007 771.820007 Volume Date 2012-01-03 7400800 2012-01-04 5765200 2012-01-05 6608400 2012-01-06 5420700 2012-01-09 11720900 ... ... 2016-12-23 623400 2016-12-27 789100 2016-12-28 1153800 2016-12-29 742200 2016-12-30 1770000 [1258 rows x 6 columns] Open High Low Close Adj Close \ Date 2017-01-03 778.809998 789.630005 775.799988 786.140015 786.140015 2017-01-04 788.359985 791.340027 783.159973 786.900024 786.900024 2017-01-05 786.080017 794.479980 785.020020 794.020020 794.020020 2017-01-06 795.260010 807.900024 792.203979 806.150024 806.150024 2017-01-09 806.400024 809.966003 802.830017 806.650024 806.650024 ... ... ... ... ... ... 2017-04-24 851.200012 863.450012 849.859985 862.760010 862.760010 2017-04-25 865.000000 875.000000 862.809998 872.299988 872.299988 2017-04-26 874.229980 876.049988 867.747986 871.729980 871.729980 2017-04-27 873.599976 875.400024 870.380005 874.250000 874.250000 2017-04-28 910.659973 916.849976 905.770020 905.960022 905.960022 Volume Date 2017-01-03 1657300 2017-01-04 1073000 2017-01-05 1335200 2017-01-06 1640200 2017-01-09 1272400 ... ... 2017-04-24 1372500 2017-04-25 1672000 2017-04-26 1237200 2017-04-27 2026800 2017-04-28 3219500 [81 rows x 6 columns]

2、产生训练所需的特征和标签数据

X_train_set = df_train.iloc[:,4:5].values

#数据归一化

sc = MinMaxScaler()

X_train_set = sc.fit_transform(X_train_set)

def create_dataset(ds, look_back=1):

X_data, Y_data = [],[]

for i in range(len(ds)-look_back):

X_data.append(ds[i:(i+look_back), 0])

Y_data.append(ds[i+look_back, 0])

return np.array(X_data), np.array(Y_data)

look_back = 60

print("回看天数:", look_back)

# 分割成特征数据和标签数据

X_train, Y_train = create_dataset(X_train_set, look_back)

X_train

Y_train输出结果:

回看天数: 60Out[5]:

array([0.08291369, 0.07626093, 0.0815312 , ..., 0.94758974, 0.94336851, 0.92287887])

3、转换数据为(样本数,时步、特征)的张量

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

X_train.shape输出结果:

(1198, 60, 1)

4、定义LSTM模型

在编译模型中,损失函数为MSE,优化器为adam。在训练模型中,训练周期为100,批次尺寸为32。

model = Sequential()

model.add(LSTM(50, return_sequences=True,

input_shape=(X_train.shape[1], 1)))

model.add(Dropout(0.2))

model.add(LSTM(50, return_sequences=True))

model.add(Dropout(0.2))

model.add(LSTM(50))

model.add(Dropout(0.2))

model.add(Dense(1))

model.summary()

#编译模型

model.compile(loss="mse", optimizer="adam")

#训练模型

model.fit(X_train, Y_train, epochs=100, batch_size=32)输出结果:

38/38 [==============================] - 2s 46ms/step - loss: 0.0013 Epoch 94/100 38/38 [==============================] - 2s 46ms/step - loss: 0.0013 Epoch 95/100 38/38 [==============================] - 2s 47ms/step - loss: 0.0012 Epoch 96/100 38/38 [==============================] - 2s 46ms/step - loss: 0.0013 Epoch 97/100 38/38 [==============================] - 2s 46ms/step - loss: 0.0013 Epoch 98/100 38/38 [==============================] - 2s 47ms/step - loss: 0.0013 Epoch 99/100 38/38 [==============================] - 2s 46ms/step - loss: 0.0012 Epoch 100/100 38/38 [==============================] - 2s 46ms/step - loss: 0.0013

5、使用已经训练好的LSTM模型预测股价

测试集为2017年1月到3月的股价,因为使用的是前60天的股价数据,使用预测的是4月份股价 。

X_test_set = df_test.iloc[:,4:5].values

# 产生标签数据

_, Y_test = create_dataset(X_test_set, look_back)

#特征数据和标准化

X_test_s = sc.transform(X_test_set)

X_test,_ = create_dataset(X_test_s, look_back)

# 转换成(样本数, 时步, 特征)张量

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

X_test_pred = model.predict(X_test)

# 将预测值转换回股价

X_test_pred_price = sc.inverse_transform(X_test_pred)

X_test_pred_price输出结果:

array([[814.5596 ], [819.2384 ], [821.1239 ], [823.5624 ], [824.0013 ], [822.3476 ], [819.3523 ], [816.00055], [813.82117], [812.62726], [812.6262 ], [812.9471 ], [817.2544 ], [821.539 ], [824.44244], [826.5891 ], [828.0157 ], [834.4217 ], [843.3087 ], [849.4051 ], [852.694 ]], dtype=float32)

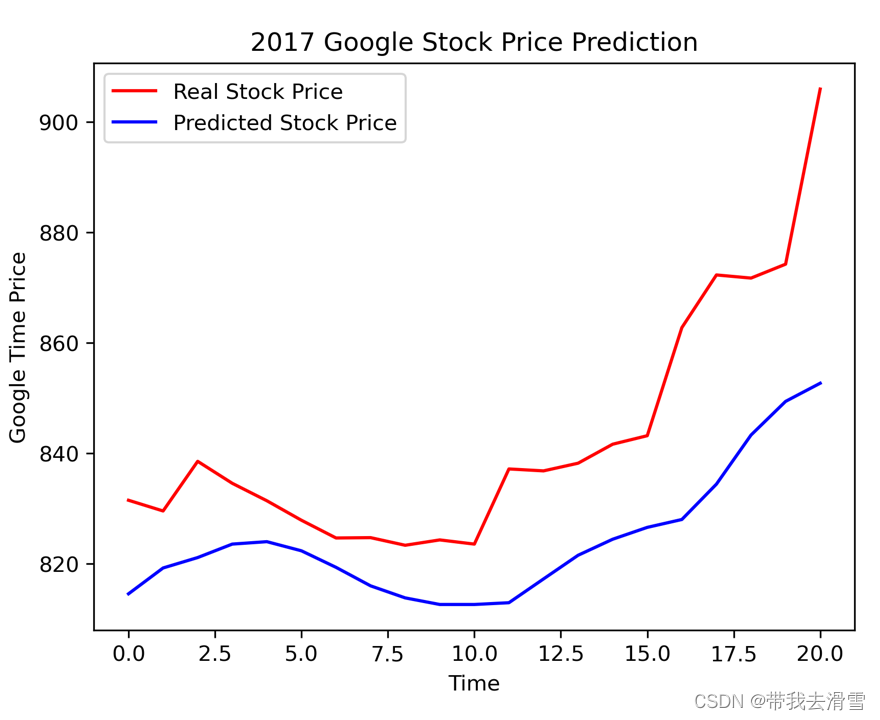

6、绘制真实股价与预测股价的对比图

import matplotlib.pyplot as plt

plt.plot(Y_test, color="red", label="Real Stock Price")

plt.plot(X_test_pred_price, color="blue", label="Predicted Stock Price")

plt.title("2017 Google Stock Price Prediction")

plt.xlabel("Time")

plt.ylabel("Google Time Price")

plt.legend()

plt.savefig("E:\工作\硕士\博客\博客37-/squares1.png",

bbox_inches ="tight",

pad_inches = 1,

transparent = True,

facecolor ="w",

edgecolor ='w',

dpi=300,

orientation ='landscape')输出结果:

更多优质内容持续发布中,请移步主页查看。

点赞+关注,下次不迷路!