Jupyter Notebook 代码连接:

machine_learning_demo

machine_learning_ensembles

Step 1: Imports and Configuration

import pandas as pd

import numpy as np

import copy

import json

import pickle

import joblib

import lightgbm as lgb

import optuna

import warnings

import gc

from sklearn.metrics import roc_curve, roc_auc_score, recall_score, accuracy_score, fbeta_score, precision_score

from sklearn.model_selection import train_test_split, cross_val_score, KFold

from sklearn.base import clone

import matplotlib.pyplot as plt

import seaborn as sns

# Setting configuration.

pd.set_option('display.float_format', lambda x: '%.5f' %x)

warnings.filterwarnings('ignore')

sns.set_style('whitegrid')

optuna.logging.set_verbosity(optuna.logging.WARNING)

SEED = 42

Step 2: Load the datasets

print('Loading data...')

path = '../datasets/Home-Credit-Default-Risk/'

df = pd.read_csv(path + 'selected_data.csv', index_col='SK_ID_CURR')

Loading data...

定义帮助节省内存的函数

def convert_dtypes(df, verbose=True):

original_memory = df.memory_usage().sum()

df = df.apply(pd.to_numeric, errors='ignore')

# Convert booleans to integers

boolean_features = df.select_dtypes(bool).columns.tolist()

df[boolean_features] = df[boolean_features].astype(np.int32)

# Convert objects to category

object_features = df.select_dtypes(object).columns.tolist()

df[object_features] = df[object_features].astype('category')

# Float64 to float32

float_features = df.select_dtypes(float).columns.tolist()

df[float_features] = df[float_features].astype(np.float32)

# Int64 to int32

int_features = df.select_dtypes(int).columns.tolist()

df[int_features] = df[int_features].astype(np.int32)

new_memory = df.memory_usage().sum()

if verbose:

print(f'Original Memory Usage: {round(original_memory / 1e9, 2)} gb.')

print(f'New Memory Usage: {round(new_memory / 1e9, 2)} gb.')

return df

print("Training dataset shape: ", df.shape)

Training dataset shape: (307511, 836)

df = convert_dtypes(df)

Original Memory Usage: 2.06 gb.

New Memory Usage: 1.0 gb.

df.dtypes.value_counts()

float32 796

int32 7

category 3

category 3

category 3

category 3

category 3

category 2

category 2

category 2

category 1

category 1

category 1

category 1

category 1

category 1

category 1

category 1

category 1

category 1

category 1

category 1

Name: count, dtype: int64

Step 3: Data preprocessing

# Check if the data is unbalanced

df["TARGET"].value_counts()

TARGET

0 282686

1 24825

Name: count, dtype: int64

数据集存在轻微的样本不平衡,我们接下来测试几种处理方法,来提高模型表现。

先定义评估函数

def timer(func):

import time

import functools

def strfdelta(tdelta, fmt):

hours, remainder = divmod(tdelta, 3600)

minutes, seconds = divmod(remainder, 60)

return fmt.format(hours, minutes, seconds)

@functools.wraps(func)

def wrapper(*args, **kwargs):

click = time.time()

result = func(*args, **kwargs)

delta = strfdelta(time.time() - click, "{:.0f} hours {:.0f} minutes {:.0f} seconds")

print(f"{func.__name__} cost time {delta}")

return result

return wrapper

# Define a cross validation strategy

# We use the cross_val_score function of Sklearn.

# However this function has not a shuffle attribute, we add then one line of code,

# in order to shuffle the dataset prior to cross-validation

@timer

def evaluate(model, X, y, n_folds = 5, params=None):

kf = KFold(n_folds, shuffle=True, random_state=SEED).get_n_splits(X)

scores = cross_val_score(

model,

X,

y,

scoring="roc_auc",

cv = kf,

verbose=1,

params=params

)

print(f"valid auc: {scores.mean():.3f} +/- {scores.std():.3f}")

return scores.mean()

Split data

留25%作为模型的验证集

# Split data into training and testing sets

X_train, X_valid, y_train, y_valid = train_test_split(

df.drop(columns="TARGET"),

df["TARGET"],

test_size=0.25,

random_state=SEED

)

print("X_train shape:", X_train.shape)

print('train:', y_train.value_counts(), sep='\n')

print('valid:', y_valid.value_counts(), sep='\n')

X_train shape: (230633, 835)

train:

TARGET

0 211999

1 18634

Name: count, dtype: int64

valid:

TARGET

0 70687

1 6191

Name: count, dtype: int64

del df

gc.collect()

# Specific feature names and categorical features

feature_name = X_train.columns.tolist()

categorical_feature = X_train.select_dtypes('category').columns.tolist()

from sklearn.preprocessing import OneHotEncoder

from sklearn.compose import make_column_transformer

# Encode categorical features

encoder = make_column_transformer(

(OneHotEncoder(

drop='if_binary',

min_frequency=0.02,

max_categories=20,

sparse_output=False,

handle_unknown='ignore'

), categorical_feature),

remainder='passthrough',

verbose_feature_names_out=False,

verbose=True

)

print('fitting...')

encoder.fit(X_train)

print('encoding...')

train_dummies = encoder.transform(X_train)

valid_dummies = encoder.transform(X_valid)

print('train data shape:', X_train.shape)

fitting...

[ColumnTransformer] . (1 of 2) Processing onehotencoder, total= 4.2s

[ColumnTransformer] ..... (2 of 2) Processing remainder, total= 0.0s

encoding...

train data shape: (230633, 835)

model 1: Use default parameters

model = lgb.LGBMClassifier(

boosting_type='gbdt',

objective='binary',

metric='auc',

n_estimators=500,

random_state=SEED,

verbose=0

)

fit_params = dict(

callbacks = [lgb.early_stopping(20)],

eval_set = [(train_dummies, y_train), (valid_dummies, y_valid)]

)

score = evaluate(model, train_dummies, y_train, params=fit_params)

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[147] valid_0's auc: 0.860844 valid_1's auc: 0.778985

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[99] valid_0's auc: 0.836905 valid_1's auc: 0.777066

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[121] valid_0's auc: 0.846901 valid_1's auc: 0.777927

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[118] valid_0's auc: 0.846341 valid_1's auc: 0.778487

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[114] valid_0's auc: 0.845653 valid_1's auc: 0.776624

valid auc: 0.779 +/- 0.001

evaluate cost time 0 hours 1 minutes 57 seconds

model 2: Set class weight

model2 = clone(model) # Construct a new unfitted estimator with the same parameters.

model2.set_params(class_weight='balanced')

score = evaluate(model2, train_dummies, y_train, params=fit_params)

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[122] valid_0's auc: 0.843105 valid_1's auc: 0.780157

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[95] valid_0's auc: 0.831016 valid_1's auc: 0.780049

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[107] valid_0's auc: 0.835709 valid_1's auc: 0.779769

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[159] valid_0's auc: 0.856821 valid_1's auc: 0.781057

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[138] valid_0's auc: 0.848312 valid_1's auc: 0.779905

valid auc: 0.780 +/- 0.002

evaluate cost time 0 hours 2 minutes 20 seconds

设置 is_unbalance=True 后,模型有所改善。

model 3: SMOTE

from imblearn.over_sampling import SMOTE

import imblearn

X_balanced, y_balanced = SMOTE(random_state=SEED).fit_resample(train_dummies, y_train)

print('balanced train data shape:', X_balanced.shape)

score = evaluate(clone(model), X_balanced, y_balanced, params=fit_params)

balanced train data shape: (423998, 990)

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[64] valid_0's auc: 0.726936 valid_1's auc: 0.7216

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[138] valid_0's auc: 0.834743 valid_1's auc: 0.780546

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[167] valid_0's auc: 0.849441 valid_1's auc: 0.782093

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[140] valid_0's auc: 0.834219 valid_1's auc: 0.780796

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[166] valid_0's auc: 0.848353 valid_1's auc: 0.780799

valid auc: 0.976 +/- 0.048

evaluate cost time 0 hours 5 minutes 46 seconds

model 4: Ensemble method

from imblearn.ensemble import BalancedRandomForestClassifier

model4 = BalancedRandomForestClassifier(

n_estimators=100,

max_depth=5,

random_state=SEED,

verbose=1

)

score = evaluate(model4, train_dummies, y_train)

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 7.3s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 0.1s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 7.2s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 0.1s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 7.2s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 0.2s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 7.3s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 0.2s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 7.1s

[Parallel(n_jobs=1)]: Done 49 tasks | elapsed: 0.1s

valid auc: 0.738 +/- 0.002

evaluate cost time 0 hours 1 minutes 21 seconds

model 5: FocalLoss

from focal_loss import BinaryFocalLoss # self-define loss function

focalloss = BinaryFocalLoss(alpha=0.9, gamma=0.05)

model5 = clone(model)

model5.set_params(objective = focalloss.objective)

fit_params['eval_metric'] = focalloss.evaluate

score = evaluate(model5, train_dummies, y_train, params=fit_params)

[LightGBM] [Info] Using self-defined objective function

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[116] valid_0's auc: 0.840709 valid_0's focal_loss: 0.0792912 valid_1's auc: 0.780966 valid_1's focal_loss: 0.0886921

[LightGBM] [Info] Using self-defined objective function

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[87] valid_0's auc: 0.82691 valid_0's focal_loss: 0.0816416 valid_1's auc: 0.779874 valid_1's focal_loss: 0.0888508

[LightGBM] [Info] Using self-defined objective function

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[101] valid_0's auc: 0.832985 valid_0's focal_loss: 0.0805644 valid_1's auc: 0.779294 valid_1's focal_loss: 0.0889485

[LightGBM] [Info] Using self-defined objective function

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[87] valid_0's auc: 0.827538 valid_0's focal_loss: 0.0816012 valid_1's auc: 0.78189 valid_1's focal_loss: 0.0885146

[LightGBM] [Info] Using self-defined objective function

Training until validation scores don't improve for 20 rounds

Early stopping, best iteration is:

[119] valid_0's auc: 0.840904 valid_0's focal_loss: 0.0792486 valid_1's auc: 0.781548 valid_1's focal_loss: 0.0886565

valid auc: nan +/- nan

evaluate cost time 0 hours 2 minutes 16 seconds

自定义FocalLoss损失函数后,表现不错

del train_dummies, valid_dummies

gc.collect()

Step 4: Hyperparameter Tuning

超参数调优算法主要有网格搜索(Grid Search),随机搜索(Randomized Search)和贝叶斯优化(Bayesian Optimization),本文采用贝叶斯优化。

本章准备使用LightGBM原生接口,需要创建 lightgbm 原生数据集

# Create Dataset object for lightgbm

dtrain = lgb.Dataset(

X_train, label=y_train,

free_raw_data=True

)

# In LightGBM, the validation data should be aligned with training data.

# if you want to re-use data, remember to set free_raw_data=False

dvalid = lgb.Dataset(

X_valid, label=y_valid,

reference=dtrain,

free_raw_data=True

)

超参数和目标函数设置

# Here we use Optuna

# define the search space and the objecive function

def objective(trial):

# LightGBM can use a dictionary to set Parameters.

params = dict(

boosting_type = 'gbdt',

objective = 'binary',

metric = 'auc',

is_unbalance = True,

num_boost_round = trial.suggest_int("num_boost_round", 50, 2000, step=50),

learning_rate = trial.suggest_float("learning_rate", 1e-4, 10, log=True),

max_depth = trial.suggest_int("max_depth", 2, 10),

feature_fraction = trial.suggest_float("feature_fraction", 0.2, 1.0),

bagging_fraction = trial.suggest_float("bagging_fraction", 0.2, 1.0),

bagging_freq = 5,

lambda_l1 = trial.suggest_float("lambda_l1", 1e-4, 1e2, log=True),

lambda_l2 = trial.suggest_float("lambda_l2", 1e-4, 1e2, log=True),

random_state = SEED,

verbosity = -1

)

# Perform the cross-validation with given parameters.

eval_results = lgb.cv(

params,

dtrain,

nfold = 5,

shuffle = True,

feature_name = feature_name,

categorical_feature = categorical_feature,

callbacks=[lgb.early_stopping(20)]

)

return eval_results['valid auc-mean'][-1]

贝叶斯优化

# Bayesian optimization

# create a study object.

study = optuna.create_study(

study_name = 'lightgbm-study', # Unique identifier of the study.

direction = 'maximize'

)

# Invoke optimization of the objective function.

study.optimize(

objective,

n_trials = 100,

timeout = 7200,

gc_after_trial = True,

show_progress_bar = True

)

joblib.dump(study, path + "lightgbm-study.pkl")

study = joblib.load(path + "lightgbm-study.pkl")

print("Best trial until now:")

print(" Value: ", study.best_trial.value)

print(" Params: ")

for key, value in study.best_trial.params.items():

print(f" {key}: {value}")

Best trial until now:

Value: 0.785777090367696

Params:

num_boost_round: 1000

learning_rate: 0.029182324488925142

max_depth: 8

feature_fraction: 0.902981862669475

bagging_fraction: 0.9853966386414182

lambda_l1: 73.55650874339202

lambda_l2: 6.572289325673235

# Continue to study

study.optimize(

objective,

n_trials = 100,

timeout = 7200,

gc_after_trial = True,

show_progress_bar = True

)

print("Number of finished trials: ", len(study.trials))

print("Best trial until now:")

print(" Best value: ", study.best_trial.value)

print(" Best params: ")

for key, value in study.best_trial.params.items():

print(f" {key}: {value}")

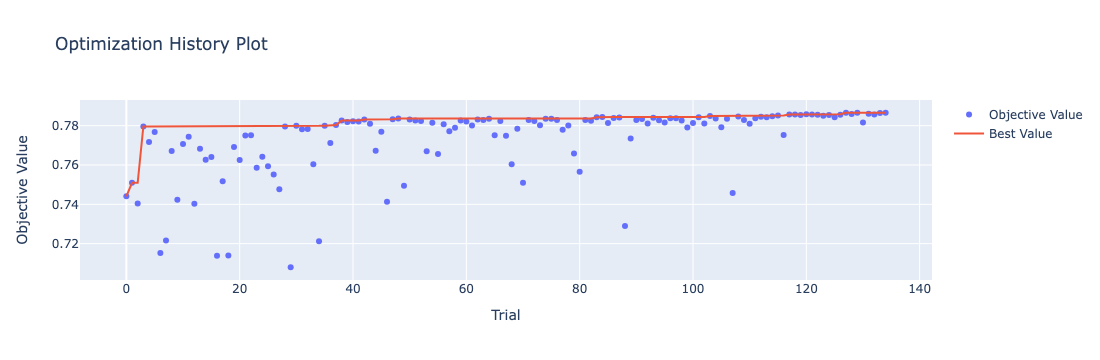

Number of finished trials: 135

Best trial until now:

Best value: 0.7865747325768904

Best params:

num_boost_round: 1300

learning_rate: 0.015480784915810246

max_depth: 8

feature_fraction: 0.3519165350962246

bagging_fraction: 0.9999568798413535

lambda_l1: 65.08840723355036

lambda_l2: 15.024421566966097

可视化

绘制优化过程曲线

optuna.visualization.plot_optimization_history(study)

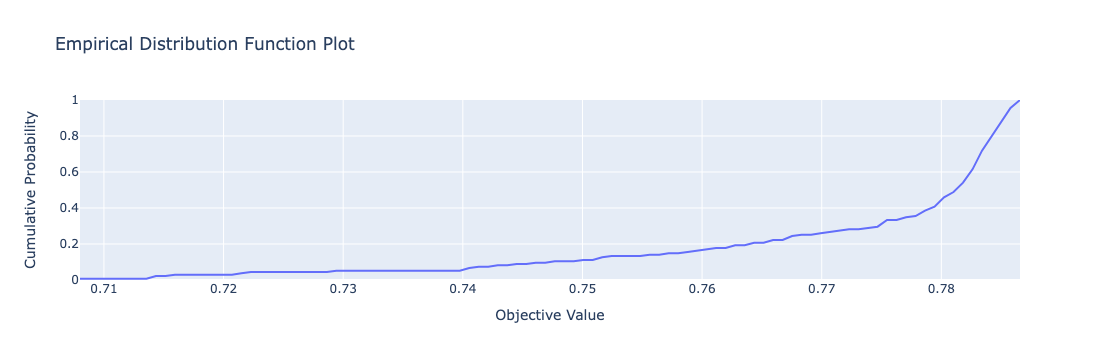

绘制study目标值的edf

optuna.visualization.plot_edf(study)

Step 5: Training

训练

本节准备使用LightGBM原生接口,需要创建 lightgbm 原生数据集

# Create Dataset object for lightgbm

dtrain = lgb.Dataset(

X_train, label=y_train,

free_raw_data=True

)

# In LightGBM, the validation data should be aligned with training data.

# if you want to re-use data, remember to set free_raw_data=False

dvalid = lgb.Dataset(

X_valid, label=y_valid,

reference=dtrain,

free_raw_data=True

)

print('Starting training...')

best_params = dict(

boosting_type = 'gbdt',

objective = 'binary',

metric = 'auc',

is_unbalance = True,

num_boost_round = 1300,

learning_rate = 0.015480784915810246,

max_depth = 8,

feature_fraction = 0.3519165350962246,

bagging_fraction = 0.9999568798413535,

lambda_l1 = 65.08840723355036,

lambda_l2 = 15.024421566966097,

subsample_freq = 5,

random_state = SEED,

verbosity = 0

)

eval_results = {} # to record eval results for plotting

callbacks = [

lgb.log_evaluation(period=100),

lgb.early_stopping(stopping_rounds=20),

lgb.record_evaluation(eval_results)

]

# Training

bst = lgb.train(

best_params,

dtrain,

feature_name = feature_name,

categorical_feature = categorical_feature,

valid_sets = [dtrain, dvalid],

callbacks = callbacks

)

Starting training...

[LightGBM] [Warning] Accuracy may be bad since you didn't explicitly set num_leaves OR 2^max_depth > num_leaves. (num_leaves=31).

[LightGBM] [Warning] Accuracy may be bad since you didn't explicitly set num_leaves OR 2^max_depth > num_leaves. (num_leaves=31).

[LightGBM] [Warning] Found whitespace in feature_names, replace with underlines

[LightGBM] [Warning] Accuracy may be bad since you didn't explicitly set num_leaves OR 2^max_depth > num_leaves. (num_leaves=31).

[LightGBM] [Warning] Accuracy may be bad since you didn't explicitly set num_leaves OR 2^max_depth > num_leaves. (num_leaves=31).

[LightGBM] [Warning] Found whitespace in feature_names, replace with underlines

[LightGBM] [Warning] Accuracy may be bad since you didn't explicitly set num_leaves OR 2^max_depth > num_leaves. (num_leaves=31).

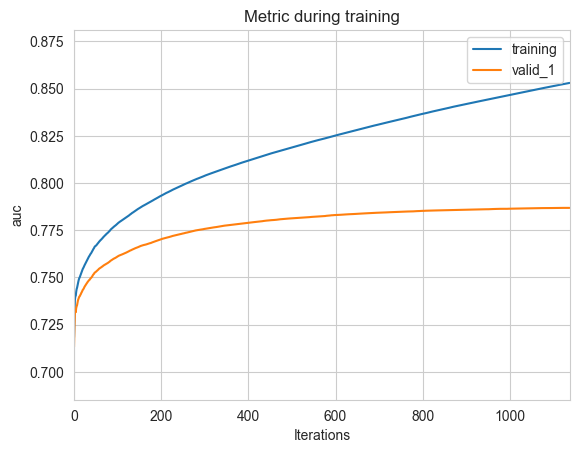

Training until validation scores don't improve for 20 rounds

[100] training's auc: 0.77831 valid_1's auc: 0.760952

[200] training's auc: 0.793115 valid_1's auc: 0.770076

[300] training's auc: 0.803729 valid_1's auc: 0.775631

[400] training's auc: 0.811797 valid_1's auc: 0.778893

[500] training's auc: 0.818789 valid_1's auc: 0.78126

[600] training's auc: 0.825071 valid_1's auc: 0.782986

[700] training's auc: 0.830958 valid_1's auc: 0.784242

[800] training's auc: 0.836567 valid_1's auc: 0.785216

[900] training's auc: 0.841761 valid_1's auc: 0.785837

[1000] training's auc: 0.846603 valid_1's auc: 0.786335

[1100] training's auc: 0.851281 valid_1's auc: 0.786744

Early stopping, best iteration is:

[1118] training's auc: 0.852112 valid_1's auc: 0.786804

可视化

# Plotting metrics recorded during training

ax = lgb.plot_metric(eval_results, metric='auc')

plt.show()

Step 6: Evaluating

模型得分

def get_adjusted_prediction(y_score, threshold=0.5):

y_pred = y_score.copy()

y_pred[y_score>=threshold] = 1

y_pred[y_score< threshold] = 0

return y_pred

def classification_report(model, X, y):

from sklearn.metrics import balanced_accuracy_score

report = {}

y_true = y

y_score = model.predict(X)

if y_score.ndim >= 2:

y_pred = np.argmax(y_score)

else:

y_pred = (y_score > 0.5).astype(int)

fpr, tpr, thresholds = roc_curve(y_true, y_score)

idx = (tpr - fpr).argmax()

adjusted_threshold = thresholds[idx]

adjusted_y_pred = (y_score > adjusted_threshold).astype(int)

return {

'y_pred': y_pred,

'y_score': y_score,

'fpr': fpr,

'tpr': tpr,

'thresholds': thresholds,

'ks': (tpr - fpr).max(),

'auc': roc_auc_score(y_true, y_score),

'accuracy': accuracy_score(y_true, y_pred),

'balanced_accuracy_score': balanced_accuracy_score(y_true, y_pred),

'precision': precision_score(y_true, y_pred),

'recall': recall_score(y_true, y_pred),

'f1-score': fbeta_score(y_true, y_pred, beta=1),

'adjusted_threshold': adjusted_threshold,

'adjusted_accuracy': accuracy_score(y_true, adjusted_y_pred)

}

# the model performance

train_report = classification_report(bst, X_train, y_train)

valid_report = classification_report(bst, X_valid, y_valid)

for label, stats in [('train data', train_report), ('valid data', valid_report)]:

print(label, ":")

print(

f"auc: {stats['auc']:.5f}",

f"accuracy: {stats['accuracy']:.5f}",

f"balanced_accuracy_score: {stats['balanced_accuracy_score']:.5f}",

f"adjusted_accuracy(threshold = {stats['adjusted_threshold']:.4f}): {stats['adjusted_accuracy']:.5f}",

f"recall: {stats['recall']:.5f}",

sep = '\n\t'

)

train data :

auc: 0.85211

accuracy: 0.75527

balanced_accuracy_score: 0.77060

adjusted_accuracy(threshold = 0.4885): 0.74530

recall: 0.78888

valid data :

auc: 0.78680

accuracy: 0.73706

balanced_accuracy_score: 0.71237

adjusted_accuracy(threshold = 0.4526): 0.69454

recall: 0.68293

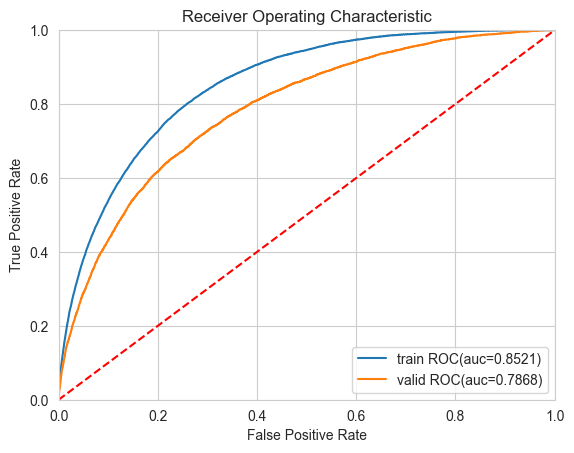

ROC曲线

# Plot ROC curve

def plot_roc_curve(fprs, tprs, labels):

from sklearn import metrics

plt.figure()

plt.title('Receiver Operating Characteristic')

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.plot([0, 1], [0, 1],'r--')

plt.xlim([0, 1])

plt.ylim([0, 1])

# Plotting ROC and computing AUC scores

for fpr, tpr, label in zip(fprs, tprs, labels):

auc = metrics.auc(fpr, tpr)

plt.plot(fpr, tpr, label = f"{label} ROC(auc={auc:.4f})")

plt.legend(loc = 'lower right')

plot_roc_curve(

fprs = (train_report['fpr'], valid_report['fpr']),

tprs = (train_report['tpr'], valid_report['tpr']),

labels = ('train', 'valid')

)

模型稳定性

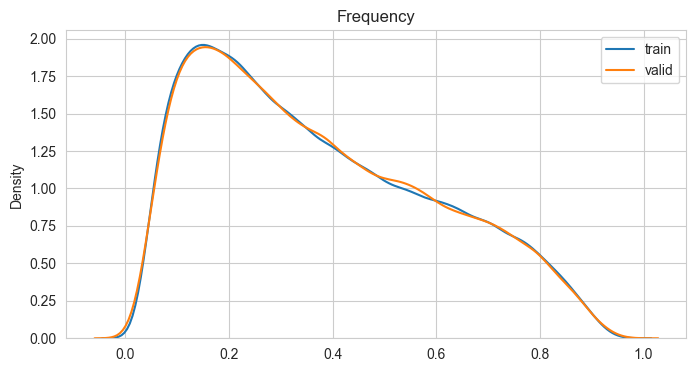

PSI(Population Stability Index)指标反映了实际分布(actual)与预期分布(expected)的差异。在建模中,我们常用来筛选特征变量、评估模型稳定性。其中,在建模时通常以训练样本(In the Sample, INS)作为预期分布,而验证样本在各分数段的分布通常作为实际分布。验证样本一般包括样本外(Out of Sample, OOS)和跨时间样本(Out of Time, OOT)。

风控模型常用PSI衡量模型的稳定性。

def calc_psi(expected, actual, n_bins=10):

'''

Calculate the PSI (Population Stability Index) for two vectors.

Args:

expected: array-like, represents the expected distribution.

actual: array-like, represents the actual distribution.

bins: int, the number of bins to use in the histogram.

Returns:

float, the PSI value.

'''

# Calculate the expected frequencies in each bin

buckets, bins = pd.qcut(expected, n_bins, retbins=True, duplicates='drop')

expected_freq = buckets.value_counts()

expected_freq = expected_freq / expected_freq.sum()

# Calculate the actual frequencies in each bin

bins = [-np.inf] + list(bins)[1: -1] + [np.inf]

actual_freq = pd.cut(actual, bins).value_counts()

actual_freq = actual_freq / actual_freq.sum()

# Calculate PSI

psi = (actual_freq - expected_freq) * np.log(actual_freq / expected_freq)

return psi.sum()

psi = calc_psi(train_report['y_score'], valid_report['y_score'])

print("PSI:", psi)

PSI: 0.00019890720303521737

绘制实际分布与预期分布曲线

plt.figure(figsize=(8, 4))

sns.kdeplot(x=train_report['y_score'], label='train')

sns.kdeplot(x=valid_report['y_score'], label='valid')

plt.legend(loc='best')

plt.title(label = 'Frequency', loc ='center')

验证集正负样本分布曲线

valid_pred = pd.DataFrame({'score': valid_report['y_score'], 'target': y_valid})

plt.figure(figsize=(8, 4))

sns.kdeplot(data=valid_pred, x='score', hue='target', common_norm=False)

plt.title(label = 'Frequency', loc ='center')

验证集正负样本累积分布

plt.figure(figsize=(8, 4))

sns.kdeplot(data=valid_pred, x='score', hue='target', common_norm=False, cumulative=True)

plt.title(label = 'Cumulative', loc ='center')

Step 7: Show feature importance

feature_imp = pd.Series(

bst.feature_importance(),

index=bst.feature_name()

).sort_values(ascending=False)

print(feature_imp.head(20))

feature_imp.to_excel(path + 'feature_importance.xlsx')

AMT_ANNUITY_/_AMT_CREDIT 776

MODE(previous.PRODUCT_COMBINATION) 590

MODE(installments.previous.PRODUCT_COMBINATION) 475

MODE(cash.previous.PRODUCT_COMBINATION) 355

EXT_SOURCE_2_+_EXT_SOURCE_3 312

MAX(bureau.DAYS_CREDIT_ENDDATE) 296

MAX(bureau.DAYS_CREDIT) 281

MODE(previous.NAME_GOODS_CATEGORY) 274

MODE(installments.previous.NAME_GOODS_CATEGORY) 270

MEAN(bureau.AMT_CREDIT_SUM_DEBT) 252

MODE(cash.previous.NAME_GOODS_CATEGORY) 248

AMT_GOODS_PRICE_/_AMT_ANNUITY 232

MEAN(previous.MEAN(cash.CNT_INSTALMENT_FUTURE)) 210

frequency(CODE_GENDER_M)_by(EXT_SOURCE_1) 196

AMT_CREDIT_-_AMT_GOODS_PRICE 195

SUM(bureau.AMT_CREDIT_SUM) 192

SUM(bureau.AMT_CREDIT_MAX_OVERDUE) 191

EXT_SOURCE_1_/_DAYS_BIRTH 182

MAX(cash.previous.DAYS_LAST_DUE_1ST_VERSION) 178

DAYS_BIRTH_/_EXT_SOURCE_1 176

dtype: int32

# Plotting feature importances

ax = lgb.plot_importance(bst, max_num_features=20)

plt.show()

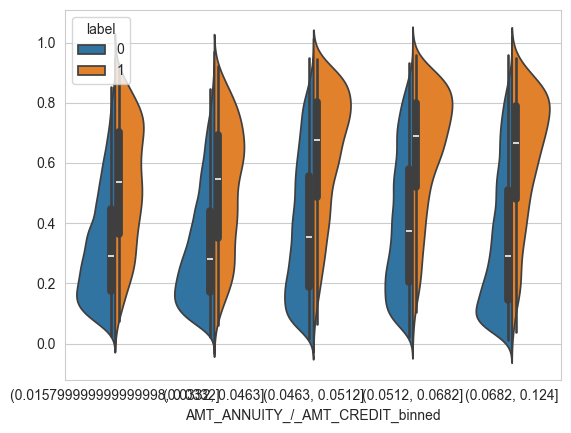

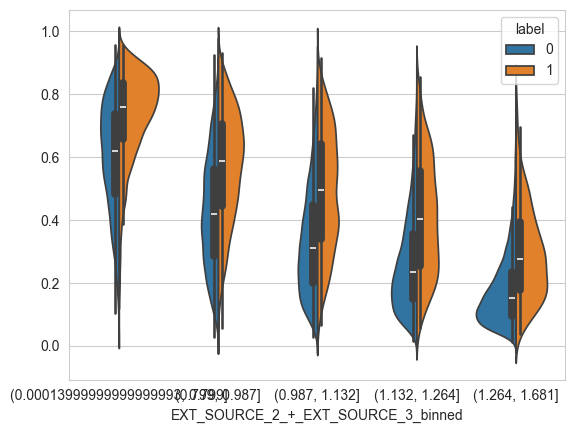

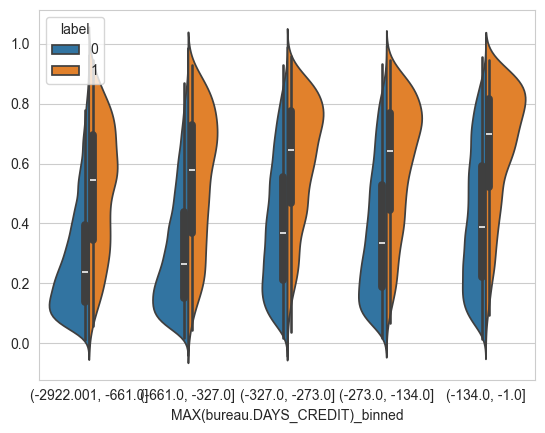

观察重点特征的分布

X_valid.columns = X_valid.columns.str.replace(' ', '_')

for col in feature_imp.index[:10]:

table = pd.DataFrame({col: X_valid[col], 'label': y_valid})

if table[col].dtype in [np.float32, np.int32]:

table[f'{col}_binned'] = pd.qcut(table[col], 5, duplicates='drop')

else:

table[f'{col}_binned'] = table[col]

print(table.pivot_table(

index=f'{col}_binned',

columns='label',

values='label',

aggfunc='count')

)

if table[f'{col}_binned'].nunique() <= 5:

sns.violinplot(

data=table,

x=f'{col}_binned',

y=valid_report['y_score'],

hue='label',

split=True

)

plt.show()

label 0 1

AMT_ANNUITY_/_AMT_CREDIT_binned

(0.015799999999999998, 0.0332] 14353 1039

(0.0332, 0.0463] 14392 974

(0.0463, 0.0512] 13906 1499

(0.0512, 0.0682] 13890 1450

(0.0682, 0.124] 14146 1229

label 0 1

MODE(previous.PRODUCT_COMBINATION)_binned

Card Street 6497 729

Card X-Sell 3161 274

Cash 12431 1234

Cash Street: high 2147 240

Cash Street: low 918 81

Cash Street: middle 910 91

Cash X-Sell: high 1695 207

Cash X-Sell: low 2944 169

Cash X-Sell: middle 3851 323

POS household with interest 17801 1333

POS household without interest 3204 205

POS industry with interest 4379 282

POS industry without interest 474 17

POS mobile with interest 8690 875

POS mobile without interest 685 54

POS other with interest 816 73

POS others without interest 84 4

label 0 1

MODE(installments.previous.PRODUCT_COMBINATION)...

Card Street 4039 472

Card X-Sell 5686 628

Cash Street: high 2265 259

Cash Street: low 903 77

Cash Street: middle 1300 128

Cash X-Sell: high 2132 251

Cash X-Sell: low 4010 193

Cash X-Sell: middle 5394 394

POS household with interest 19706 1657

POS household without interest 5942 412

POS industry with interest 6274 424

POS industry without interest 828 31

POS mobile with interest 9593 1032

POS mobile without interest 1086 97

POS other with interest 1369 127

POS others without interest 160 9

label 0 1

MODE(cash.previous.PRODUCT_COMBINATION)_binned

Cash Street: high 2695 340

Cash Street: low 1053 95

Cash Street: middle 1554 171

Cash X-Sell: high 2544 315

Cash X-Sell: low 4653 258

Cash X-Sell: middle 6635 496

POS household with interest 22600 1994

POS household without interest 6767 494

POS industry with interest 6970 493

POS industry without interest 923 35

POS mobile with interest 11399 1241

POS mobile without interest 1219 112

POS other with interest 1498 136

POS others without interest 177 11

label 0 1

EXT_SOURCE_2_+_EXT_SOURCE_3_binned

(0.00013999999999999993, 0.799] 12583 2793

(0.799, 0.987] 13994 1381

(0.987, 1.132] 14411 965

(1.132, 1.264] 14688 687

(1.264, 1.681] 15011 365

label 0 1

MAX(bureau.DAYS_CREDIT_ENDDATE)_binned

(-41875.001, 80.0] 14445 941

(80.0, 823.0] 14358 1014

(823.0, 983.0] 13918 1453

(983.0, 1735.0] 13997 1399

(1735.0, 31199.0] 13969 1384

label 0 1

MAX(bureau.DAYS_CREDIT)_binned

(-2922.001, -661.0] 14554 825

(-661.0, -327.0] 14371 1031

(-327.0, -273.0] 13949 1408

(-273.0, -134.0] 14068 1326

(-134.0, -1.0] 13745 1601

label 0 1

MODE(previous.NAME_GOODS_CATEGORY)_binned

Additional Service 10 0

Audio/Video 6458 469

Auto Accessories 467 42

Clothing and Accessories 1541 89

Computers 5827 482

Construction Materials 1432 104

Consumer Electronics 5977 422

Direct Sales 29 5

Education 13 1

Fitness 17 1

Furniture 2578 143

Gardening 129 5

Homewares 242 15

Insurance 0 0

Jewelry 247 24

Medical Supplies 256 10

Medicine 112 7

Mobile 9794 935

Office Appliances 50 2

Other 49 5

Photo / Cinema Equipment 550 56

Sport and Leisure 79 13

Tourism 78 3

Vehicles 140 12

Weapon 5 0

XNA 34607 3346

label 0 1

MODE(installments.previous.NAME_GOODS_CATEGORY)...

Additional Service 9 0

Animals 1 0

Audio/Video 6092 497

Auto Accessories 347 51

Clothing and Accessories 1604 88

Computers 6324 542

Construction Materials 1571 121

Consumer Electronics 7279 562

Direct Sales 13 4

Education 14 1

Fitness 22 1

Furniture 3235 208

Gardening 175 7

Homewares 363 29

Insurance 0 0

Jewelry 238 29

Medical Supplies 400 17

Medicine 162 9

Mobile 10152 1046

Office Appliances 90 9

Other 100 7

Photo / Cinema Equipment 1115 103

Sport and Leisure 150 18

Tourism 106 4

Vehicles 261 28

Weapon 6 0

XNA 30858 2810

label 0 1

MEAN(bureau.AMT_CREDIT_SUM_DEBT)_binned

(-220213.42299999998, 0.0] 16805 994

(0.0, 39052.254] 12066 886

(39052.254, 49487.143] 13928 1448

(49487.143, 148125.9] 13904 1471

(148125.9, 43650000.0] 13984 1392

Step 8: Visualize the model

# Plotting split value histogram

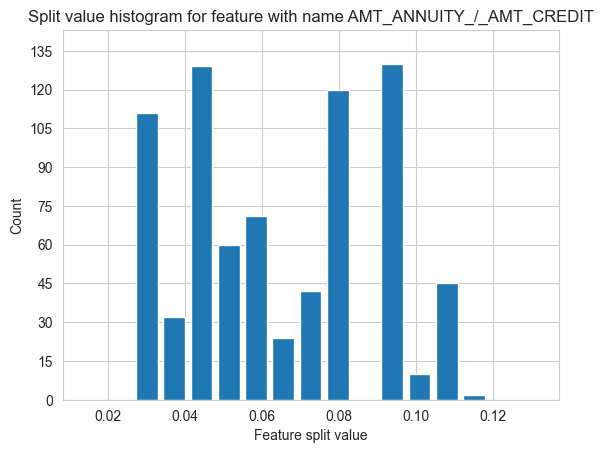

ax = lgb.plot_split_value_histogram(bst, feature='AMT_ANNUITY_/_AMT_CREDIT', bins='auto')

plt.show()

# Plotting 54th tree (one tree use categorical feature to split)

# ax = lgb.plot_tree(bst, tree_index=53, figsize=(15, 15), show_info=['split_gain'])

# plt.show()

# Plotting 54th tree with graphviz

# graph = lgb.create_tree_digraph(bst, tree_index=53, name='Tree54')

# graph.render(view=True)

Step 9: Model persistence

# Save model to file

print('Saving model...')

bst.save_model(path + 'lgb_model.txt')

Saving model...

<lightgbm.basic.Booster at 0x2c457d3a0>

Step 10: Predict

# Perform predictions

# If early stopping is enabled during training, you can get predictions from the best iteration with bst.best_iteration.

predictions = bst.predict(X_valid, num_iteration=bst.best_iteration)

# Load a saved model to predict

print('Loading model to predict...')

bst = lgb.Booster(model_file=path + 'lgb_model.txt')

predictions = bst.predict(X_valid)

Loading model to predict...

# Save predictions

# predictions.to_csv('valid_predictions.csv', index=True)

Appendices: FocalLoss

import numpy as np

from scipy import optimize, special

class BinaryFocalLoss:

def __init__(self, gamma, alpha=None):

# 使用FocalLoss只需要设定以上两个参数,如果alpha=None,默认取值为1

self.alpha = alpha

self.gamma = gamma

def at(self, y):

# alpha 参数, 根据FL的定义函数,正样本权重为self.alpha,负样本权重为1 - self.alpha

if self.alpha is None:

return np.ones_like(y)

return np.where(y, self.alpha, 1 - self.alpha)

def pt(self, y, p):

# pt和p的关系

p = np.clip(p, 1e-15, 1 - 1e-15)

return np.where(y, p, 1 - p)

def __call__(self, y_true, y_pred):

# 即FL的计算公式

at = self.at(y_true)

pt = self.pt(y_true, y_pred)

return -at * (1 - pt) ** self.gamma * np.log(pt)

def grad(self, y_true, y_pred):

# 一阶导数

y = 2 * y_true - 1 # {0, 1} -> {-1, 1}

at = self.at(y_true)

pt = self.pt(y_true, y_pred)

g = self.gamma

return at * y * (1 - pt) ** g * (g * pt * np.log(pt) + pt - 1)

def hess(self, y_true, y_pred):

# 二阶导数

y = 2 * y_true - 1 # {0, 1} -> {-1, 1}

at = self.at(y_true)

pt = self.pt(y_true, y_pred)

g = self.gamma

u = at * y * (1 - pt) ** g

du = -at * y * g * (1 - pt) ** (g - 1)

v = g * pt * np.log(pt) + pt - 1

dv = g * np.log(pt) + g + 1

return (du * v + u * dv) * y * (pt * (1 - pt))

def init_score(self, y_true):

# 样本初始值寻找过程

res = optimize.minimize_scalar(

lambda p: self(y_true, p).sum(),

bounds=(0, 1),

method='bounded'

)

p = res.x

log_odds = np.log(p / (1 - p))

return log_odds

def objective(self, y_true, y_pred):

y = y_true

p = special.expit(y_pred)

return self.grad(y, p), self.hess(y, p)

def evaluate(self, y_true, y_pred):

y = y_true

p = special.expit(y_pred)

is_higher_better = False

return 'focal_loss', self(y, p).mean(), is_higher_better

def fobj(self, preds, train_data):

'''lightgbm'''

y = train_data.get_label()

p = special.expit(preds)

return self.grad(y, p), self.hess(y, p)

def feval(self, preds, train_data):

'''lightgbm'''

y = train_data.get_label()

p = special.expit(preds)

is_higher_better = False

return 'focal_loss', self(y, p).mean(), is_higher_better

class SparseCategoricalFocalLoss:

pass

Ensembles

有时候模型集成可以取得不错的效果。常用的模型集成包括:

- Votting:简单投票或加权平均

- Stacking:简单来说就是学习各个基本模型的预测值来预测最终的结果

我们初步选用 Stacking 集成学习器,采用 LogisticRegression、SVC、GaussianNB、SGDClassifier 、RandomForestClassifier、HistGradientBoostingClassifier作为基分类器。

导入必要的包

import pandas as pd

import numpy as np

import copy

import json

import pickle

import joblib

import lightgbm as lgb

import optuna

import warnings

import gc

from sklearn.ensemble import StackingClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.linear_model import SGDClassifier

from sklearn.svm import SVC

from sklearn.naive_bayes import GaussianNB

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.ensemble import HistGradientBoostingClassifier

from sklearn.model_selection import train_test_split, cross_val_score, KFold

from sklearn.metrics import roc_auc_score

from sklearn.base import clone

import matplotlib.pyplot as plt

import seaborn as sns

# Setting configuration.

pd.set_option('display.float_format', lambda x: '%.5f' %x)

warnings.filterwarnings('ignore')

sns.set_style('whitegrid')

optuna.logging.set_verbosity(optuna.logging.WARNING)

SEED = 42

创建数据集

print('Loading data...')

path = '../datasets/Home-Credit-Default-Risk/selected_data.csv'

df = pd.read_csv(path, index_col='SK_ID_CURR')

Loading data...

# Split data into training and testing sets

X_train, X_valid, y_train, y_valid = train_test_split(

df.drop(columns="TARGET"),

df["TARGET"],

test_size=0.25,

random_state=SEED

)

print("X_train shape:", X_train.shape)

print('train:', y_train.value_counts(), sep='\n')

print('valid:', y_valid.value_counts(), sep='\n')

X_train shape: (230633, 835)

train:

TARGET

0 211999

1 18634

Name: count, dtype: int64

valid:

TARGET

0 70687

1 6191

Name: count, dtype: int64

无序分类(unordered)特征原始编码对于树集成模型(tree-ensemble like XGBoost)是可用的,但对于线性回归模型(like Lasso or LogisticRegression)则必须使用one-hot重编码。因此,我们先把数据重编码。

# Specific feature names and categorical features

feature_name = X_train.columns.tolist()

categorical_feature = X_train.select_dtypes(object).columns.tolist()

from sklearn.preprocessing import OneHotEncoder

from sklearn.compose import make_column_transformer

# Encode categorical features

encoder = make_column_transformer(

(OneHotEncoder(

drop='if_binary',

min_frequency=0.02,

max_categories=20,

sparse_output=False,

handle_unknown='ignore'

), categorical_feature),

remainder='passthrough',

verbose_feature_names_out=False,

verbose=True

)

print('fitting...')

encoder.fit(X_train)

print('encoding...')

train_dummies = encoder.transform(X_train)

valid_dummies = encoder.transform(X_valid)

print('train data shape:', X_train.shape)

fitting...

[ColumnTransformer] . (1 of 2) Processing onehotencoder, total= 4.7s

[ColumnTransformer] ..... (2 of 2) Processing remainder, total= 0.0s

encoding...

train data shape: (230633, 835)

del df, X_train, X_valid

gc.collect()

2948

创建优化器

先定义一个评估函数

# Define a cross validation strategy

# We use the cross_val_score function of Sklearn.

# However this function has not a shuffle attribute, we add then one line of code,

# in order to shuffle the dataset prior to cross-validation

def evaluate(model, X, y, n_folds = 5, verbose=True):

kf = KFold(n_folds, shuffle=True, random_state=SEED).get_n_splits(X)

scores = cross_val_score(

model,

X,

y,

scoring="roc_auc",

cv = kf

)

if verbose:

print(f"valid auc: {scores.mean():.3f} +/- {scores.std():.3f}")

return scores.mean()

然后,我们定义一个优化器,对这些基分类器超参数调优。

class Objective:

estimators = (

LogisticRegression,

SGDClassifier,

GaussianNB,

RandomForestClassifier,

HistGradientBoostingClassifier

)

def __init__(self, estimator, X, y):

# assert isinstance(estimator, estimators), f"estimator must be one of {estimators}"

self.model = estimator

self.X = X

self.y = y

def __call__(self, trial):

# Create hyperparameter space

if isinstance(self.model, LogisticRegression):

search_space = dict(

class_weight = 'balanced',

C = trial.suggest_float('C', 0.01, 100.0, log=True),

l1_ratio = trial.suggest_float('l1_ratio', 0.0, 1.0) # The Elastic-Net mixing parameter, with 0 <= l1_ratio <= 1.

)

elif isinstance(self.model, SGDClassifier):

search_space = dict(

class_weight = 'balanced',

loss = trial.suggest_categorical('loss', ['hinge', 'log_loss', 'modified_huber']),

alpha = trial.suggest_float('alpha', 1e-5, 10.0, log=True),

penalty = 'elasticnet',

l1_ratio = trial.suggest_float('l1_ratio', 0.0, 1.0),

early_stopping = True

)

elif isinstance(self.model, GaussianNB):

search_space = dict(

priors = None

)

elif isinstance(self.model, RandomForestClassifier):

search_space = dict(

class_weight = 'balanced',

n_estimators = trial.suggest_int('n_estimators', 50, 500, step=50),

max_depth = trial.suggest_int('max_depth', 2, 20),

max_features = trial.suggest_float('max_features', 0.2, 0.9),

random_state = SEED

)

elif isinstance(self.model, HistGradientBoostingClassifier):

search_space = dict(

class_weight = 'balanced',

learning_rate = trial.suggest_float('learning_rate', 1e-3, 10.0, log=True),

max_iter = trial.suggest_int('max_iter', 50, 500, step=50),

max_depth = trial.suggest_int('max_depth', 2, 20),

max_features = trial.suggest_float('max_features', 0.2, 0.9),

l2_regularization = trial.suggest_float('l2_regularization', 1e-3, 10.0, log=True),

random_state = SEED,

verbose = 0

)

# Setting hyperparameters

self.model.set_params(**search_space)

# Training with 5-fold CV:

score = evaluate(self.model, self.X, self.y)

return score

超参数优化

并行执行贝叶斯优化

def timer(func):

import time

import functools

def strfdelta(tdelta, fmt):

hours, remainder = divmod(tdelta, 3600)

minutes, seconds = divmod(remainder, 60)

return fmt.format(hours, minutes, seconds)

@functools.wraps(func)

def wrapper(*args, **kwargs):

click = time.time()

result = func(*args, **kwargs)

delta = strfdelta(time.time() - click, "{:.0f} hours {:.0f} minutes {:.0f} seconds")

print(f"{func.__name__} cost time {delta}")

return result

return wrapper

# Creating a pipeline & Hyperparameter tuning

@timer

def tuning(model, X, y):

# create a study object

study = optuna.create_study(direction="maximize")

# Invoke optimization of the objective function.

objective = Objective(model, X, y)

study.optimize(

objective,

n_trials = 50,

timeout = 2400,

gc_after_trial = True,

show_progress_bar = True

)

print(model, 'best score:', study.best_value)

return study

Objective.estimators

(sklearn.linear_model._logistic.LogisticRegression,

sklearn.linear_model._stochastic_gradient.SGDClassifier,

sklearn.naive_bayes.GaussianNB,

sklearn.ensemble._forest.RandomForestClassifier,

sklearn.ensemble._hist_gradient_boosting.gradient_boosting.HistGradientBoostingClassifier)

# opt_results = []

# for model in Objective.estimators:

# study = tuning(model(), train_dummies, y_train)

# opt_results.append(study)

# print(model)

# print(study.best_trial.params)

模型训练

集成模型调优

# define the search space and the objecive function

def stacking_obj(trial):

stacking = StackingClassifier(

# The `estimators` parameter corresponds to the list of the estimators which are stacked.

estimators = [

('Logit', LogisticRegression(

class_weight = 'balanced',

C = trial.suggest_float('Logit__C', 0.01, 100.0, log=True),

l1_ratio = trial.suggest_float('Logit__l1_ratio', 0.0, 1.0) # The Elastic-Net mixing parameter, with 0 <= l1_ratio <= 1.

)),

('SGD', SGDClassifier(

class_weight = 'balanced',

loss = trial.suggest_categorical('SGD__loss', ['hinge', 'log_loss', 'modified_huber']),

alpha = trial.suggest_float('SGD__alpha', 1e-5, 10.0, log=True),

penalty = 'elasticnet',

l1_ratio = trial.suggest_float('SGD__l1_ratio', 0.0, 1.0),

early_stopping = True

)),

('GaussianNB', GaussianNB())

],

# The final_estimator will use the predictions of the estimators as input

final_estimator = LogisticRegression(

class_weight = 'balanced',

C = trial.suggest_float('final__C', 0.01, 100.0, log=True),

# The Elastic-Net mixing parameter, with 0 <= l1_ratio <= 1.

l1_ratio = trial.suggest_float('final__l1_ratio', 0.0, 1.0)

),

verbose = 1

)

score = evaluate(stacking, train_dummies, y_train, n_folds = 3)

return score

# create a study object.

study = optuna.create_study(

study_name = 'stacking-study', # Unique identifier of the study.

direction = 'maximize'

)

# Invoke optimization of the objective function.

study.optimize(

stacking_obj,

n_trials = 100,

timeout = 3600,

gc_after_trial = True,

show_progress_bar = True

)

valid auc: 0.676 +/- 0.017

valid auc: 0.669 +/- 0.021

valid auc: 0.673 +/- 0.016

valid auc: 0.451 +/- 0.121

valid auc: 0.592 +/- 0.045

valid auc: 0.666 +/- 0.017

valid auc: 0.675 +/- 0.014

valid auc: 0.666 +/- 0.021

valid auc: 0.672 +/- 0.016

valid auc: 0.667 +/- 0.021

valid auc: 0.672 +/- 0.012

joblib.dump(study, path + "stacking-study.pkl")

study = joblib.load(path + "stacking-study.pkl")

print("Best trial until now:")

print(" Value: ", study.best_trial.value)

print(" Params: ")

for key, value in study.best_trial.params.items():

print(f" {key}: {value}")

Best trial until now:

Value: 0.6761396385434888

Params:

Logit__C: 0.020329668727865235

Logit__l1_ratio: 0.5165207006926232

SGD__loss: modified_huber

SGD__alpha: 1.6638099778831132

SGD__l1_ratio: 0.7330208370976262

final__C: 14.1468564043383

final__l1_ratio: 0.4977751012657087

stacking = StackingClassifier(

# The `estimators` parameter corresponds to the list of the estimators which are stacked.

estimators = [

('Logit', LogisticRegression(

class_weight = 'balanced',

C = 0.020329668727865235,

l1_ratio = 0.5165207006926232 # The Elastic-Net mixing parameter, with 0 <= l1_ratio <= 1.

)),

('SGD', SGDClassifier(

class_weight = 'balanced',

loss = 'modified_huber',

alpha = 1.6638099778831132,

penalty = 'elasticnet',

l1_ratio = 0.7330208370976262,

early_stopping = True

)),

('GaussianNB', GaussianNB())

],

# The final_estimator will use the predictions of the estimators as input

final_estimator = LogisticRegression(

class_weight = 'balanced',

C = 14.1468564043383,

# The Elastic-Net mixing parameter, with 0 <= l1_ratio <= 1.

l1_ratio = 0.4977751012657087

),

verbose = 1

)

score = evaluate(stacking, train_dummies, y_train)

valid auc: 0.674 +/- 0.009

stacking.fit(train_dummies, y_train)

train_auc = roc_auc_score(y_train, stacking.predict_proba(train_dummies)[:, 1])

valid_auc = roc_auc_score(y_valid, stacking.predict_proba(valid_dummies)[:, 1])

print('train auc:', train_auc)

print('valid auc:', valid_auc)

train auc: 0.6753919322392181

valid auc: 0.6752015627178207